Repo, On-chain

This post was co-authored with Francesco Mangia, a quantitative researcher with experience in both DeFi and traditional finance, specializing in risk analysis, quantitative strategies, and financial infrastructure.

RWA tokenization has moved past its first chapter. The early promise was straightforward: take a real-world asset, put it on-chain, make it accessible more easily to more investor categories. In this first wave, non crypto assets’ main use cases on-chain were, on one hand, diversification for crypto whales/riches and, on the other hand, jurisdictional arbitrage - access to interesting assets for investors in jurisdictions where those assets were not easily available.

What is happening now is different. DeFi protocols are now replicating on RWA the same mechanics that made crypto-native yield farming possible, but with T-Bills and private credit underneath, essentially building leverage structures on top of these assets, layer by layer.

The goal of this post is to analyse this phenomenon, compare it to traditional leveraging structures and draw a few conclusions on the scalability of this phenomenon.

Looping Mechanics

The mechanics of looping adopted by RWA on-chain users are fairly standardised for the crypto industry: a user deposits a tokenized T-Bill on Morpho or Euler, borrows a stablecoin against it, acquires more of the same asset, and redeposits. The underlying asset is real, the yield is real, the exposure is multiplied. Nothing about this logic is new: what is new is that it runs on open, composable infrastructure with no intermediary controlling the loop.

The more structurally interesting development is one layer up. When an asset manager wraps a looping strategy into an on-chain vault, depositors receive a receipt token representing their share. That receipt is itself becoming collateral in the same lending markets - a claim on a claim, one abstraction removed from the underlying. Protocols like 3F.xyz implement this directly: a looping strategy on tokenized private credit wrapped into a vault, with the receipt token redeployable as collateral in the same markets.

This introduces an actor with no direct equivalent in traditional finance: the curator. An on-chain entity selecting collateral types, setting LTV parameters, and choosing oracles -in practice, structuring a credit product without a balance sheet or a banking license. The capital funding these strategies flows through curated vaults that abstract away execution complexity, which means the curator’s decisions about collateral quality and leverage limits are what the depositor is actually underwriting, whether or not they know it.

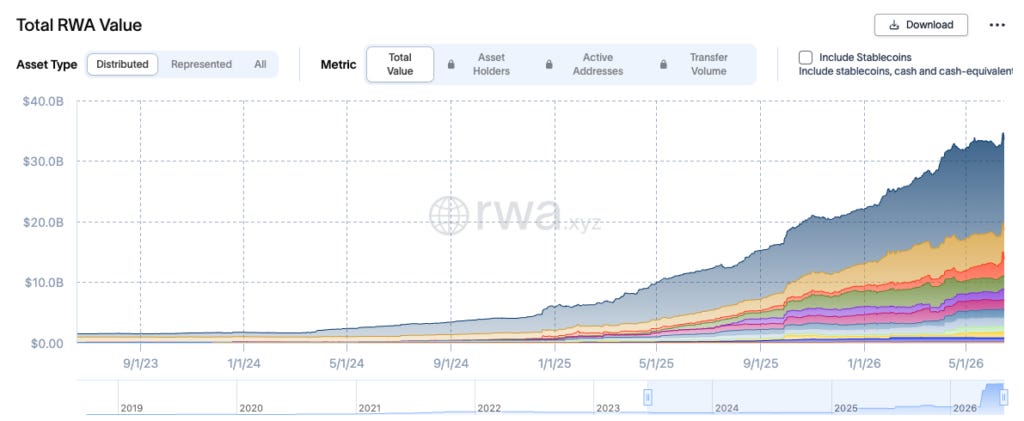

All of this is only possible because the underlying infrastructure now works at scale. Lending protocols like Morpho and Euler have grown deep enough for institutional size, oracle networks cover non-crypto-native assets with increasing reliability, and RWA TVL grew from $15 billion to over $33 billion in less than 18 months. The plumbing works, the question is what it enables.

The Same Trade, Different Rails

This type of product is not new. This loop has a direct equivalent in traditional finance: repo markets and securities lending, where institutions borrow against high-quality collateral, reinvest, and repeat.

The US repo market sits at roughly $12.6 trillion in daily exposures, the global market at around $24.7 trillion. A hedge fund deposits T-Bills as collateral, receives cash, buys more T-Bills, repeats.

The same pattern now runs on Morpho with tokenized private credit as the underlying, but there are a number of dimensions that the on-chain model solves differently, with potentially enormous benefits.

Access

The Repo market is a wholesale market. The legal minimum to open a prime brokerage account sits at $500,000 in equity, and tier-1 prime brokers work only with funds at meaningful AUM scale. GMRA documentation, credit assessment, and relationship management add friction that keeps the loop inaccessible to most capital. The yield differential, capturing the spread between a private credit return and a stablecoin borrow rate, has historically accrued entirely to institutions with the right counterparty relationships.

On-chain things are different: any permissioned wallet can run the same trade on Morpho or Euler. No minimum ticket, no relationship requirement. The LTVs are deliberately more conservative than in repo, partly because the collateral is less liquid, partly because the protocols are still building a track record. The practical effect is that a strategy structurally unavailable outside a prime brokerage relationship becomes accessible to smaller hedge funds, family offices, and sophisticated individual allocators.

Transparency

The $4.6 trillion in non-centrally-cleared bilateral Repo is the least visible segment of the market. The Fed launched a dedicated data collection initiative only in December 2024 to close this information gap. Even now, the aggregate leverage built on any single piece of collateral is not reconstructable from any single source.

On-chain, every position is public, every parameter is encoded in the smart contract, and the full leverage stack sitting on top of a given RWA is aggregable by anyone reading on-chain state. This matters most at the systemic level: for the first time it is possible to measure in real time how much of a single collateral asset is deployed across multiple protocols simultaneously. In TradFi this is not observable even by regulators.

The implications cut both ways. For regulators and risk managers, systemic concentration becomes measurable in real time without relying on voluntary reporting. For large allocators, strategy and position sizing are public by default. More structurally, concentration visible on-chain can accelerate coordinated exits in stress scenarios in ways that are harder to engineer in TradFi, where opacity slows contagion as much as it obscures risk.

Settlement

In TradFi each loop leg clears at T+1 or T+2. Building a 5x position on a T+1 asset through manual looping takes roughly 20 days to enter and another 20 to unwind, with market risk accumulating throughout. Forced deleveraging plays out over days, with human intervention at each step. On-chain, the entire loop can be constructed and unwound within minutes. For capital allocators this reduces execution risk and the cost of carrying an unwanted position.

Though, the speed of settlement comes with a huge burden: systemic fragility. Under stress in TradFi the friction of manual deleveraging slows contagion; on-chain, automated liquidations execute within a block across all affected positions simultaneously. Without intermediaries to absorb or sequence the flow, a price move in one protocol can trigger liquidations that propagate across interconnected markets faster than any circuit breaker can respond. This is amplified for RWA collateral where quarterly redemption windows or limited secondary market liquidity don’t resonate properly, with a liquidation mechanism that assumes a speed of exit the underlying asset cannot support.

Rehypothecation vs smart-contract custody

In TradFi, rehypothecation transfers legal title to the receiving counterparty, who can re-pledge the same collateral to a third party, who can re-pledge it again. Each transfer is a separate bilateral agreement, and the original owner has no visibility into how many times the asset has been reused down the chain. In the US the cap sits at 140% of client debit balance under Rule 15c3-3; in the UK there is no equivalent limit. If any counterparty in that chain becomes insolvent, the original owner is left with a claim against its estate, alongside other unsecured creditors, rather than a right to the specific asset.

On-chain, the collateral sits in the lending protocol’s smart contract, recorded against the depositor’s address. Morpho and Euler track each position individually: the contract, not a counterparty, holds the asset, and the depositor’s claim is enforced by code rather than by a chain of bilateral agreements. When the receipt token from that position is redeposited as collateral elsewhere, the original asset doesn’t move again, only a token representing a claim on it does. There is no balance sheet for the underlying RWA to disappear into if an intermediary fails, because no intermediary ever held title to begin with.

This doesn’t make on-chain leverage safer overall. Smart contract risk, oracle failure, and the illiquidity of the underlying RWA remain real, and stacking multiple layers on the same collateral concentrates that risk rather than removing it. What changes is the counterparty insolvency risk on the collateral itself, not the operational or liquidity risk sitting underneath it.

Cost of capital and rate pricing

In TradFi information asymmetry still runs the game: the borrow rate on a repo is either bilaterally negotiated or discovered through interdealer platforms like BrokerTec, where terms reflect counterparty relationships, volume history, and collateral quality assessed individually. Rates across the non-centrally-cleared bilateral segment are not uniform even for identical collateral: the OFR has documented material rate dispersion driven by participants’ private information and alternative trading opportunities, with the less liquid segments of the market subject to commercially negotiated risk management terms that can diverge significantly from best practice.

On-chain, the borrow rate is entirely algorithmic and, thus, equal for everyone. Protocols like Aave and Morpho use a kinked utilization model: the rate rises gradually up to an optimal utilization threshold, typically 80-95%, and then increases steeply to deter further borrowing and protect remaining liquidity. The rate is the same for every borrower at any given block, regardless of size or identity. What the on-chain model loses in relationship-based flexibility it gains in predictability and auditability: every parameter is visible, the curve is deterministic, and rate changes are instantaneous and global rather than negotiated transaction by transaction.

Margin and liquidation

In TradFi, when collateral value falls below the agreed threshold, the receiving party issues a margin call. Under the GMRA, collateral should be revalued daily and margin delivered on the same day or by the next business day. If the parties disagree on valuation, a formal dispute resolution process kicks in, with resolution deadlines typically set at 1pm New York time on the business day following the dispute. Throughout this process there is human intervention, bilateral negotiation, and the possibility of renegotiating terms.

On-chain there is none of this. Liquidation is automatic, executed by external liquidator bots the moment a position crosses the liquidation threshold encoded in the smart contract. There is no margin call, no dispute window, no renegotiation. For liquid crypto-native assets this works efficiently: the liquidator sells the collateral on-market and recovers the debt within the same block. For tokenized RWA collateral with quarterly redemption windows or limited secondary market liquidity, the same mechanism requires the liquidator to warehouse the risk of the underlying asset, which in stress scenarios may not be sellable at any price within the settlement window.

For allocators who run leveraged RWA positions, this is the most material operational difference from TradFi. The absence of a negotiation layer removes flexibility but also removes counterparty risk. Whether that tradeoff is favorable depends entirely on the liquidity profile of the underlying collateral.

Conclusions

The infrastructure described in this piece differs from repo in several measurable dimensions: settlement speed, position transparency, access thresholds, and liquidation mechanics. Whether the new rails will produce a structurally different system or a more efficient version of the existing one is not yet clear.

The most direct beneficiaries at this stage are allocators previously excluded by ticket size and relationship requirements: smaller hedge funds, family offices, and sophisticated individuals. For large institutions the calculus is less straightforward. The transparency that makes the system auditable also makes positioning public. The automation that removes counterparty risk also removes the negotiation flexibility that institutional desks are structured around. The operational differences from TradFi are not uniformly advantages depending on who is running the position.

The first movers are crypto-native funds and DeFi-native allocators comfortable with smart contract risk and operational complexity. The second wave, already visible, is smaller TradFi institutions attracted by yield differentials that are not accessible at equivalent ticket sizes in traditional repo. Large institutional adoption will depend on three things that are not yet in place: standardized legal frameworks for tokenized collateral, oracle infrastructure with institutional-grade reliability, and a documented track record of liquidation mechanisms performing under stress on RWA-specific collateral.

Whether the system gets that far depends on what happens first.

The first scenario is regulatory: jurisdictions conclude that the transparency and automation of on-chain leverage does not compensate for reduced supervisory control, and institutional capital follows the regulation out.

The second is endogenous: a liquidation cascade on illiquid RWA collateral produces losses large enough to discredit the model before it reaches scale, which is a plausible outcome given the structural mismatch between on-chain liquidation speed and the redemption windows of the underlying assets.

The third scenario is the most structurally interesting. The system does not fail but converges toward what it was meant to differ from: curators acquire the legal and compliance infrastructure of asset managers; vaults get wrapped into regulated fund structures and oracle providers take on the role of pricing services. The on-chain rails remain but every function built on top of them has a direct institutional equivalent, and the properties that distinguished the system from repo have been progressively absorbed into the frameworks of the industry it was built alongside. This would not be a failure in the conventional sense and it may be the most likely outcome.